Documents

DocumentsTable of Contents Back to Top

- DATES:

- ADDRESSES:

- FOR FURTHER INFORMATION CONTACT:

- SUPPLEMENTARY INFORMATION:

- I. Comments

- II. Background

- A. Statutory and Regulatory Background for the Existing Housing Goals

- B. Adjusting the Housing Goals

- C. Housing Goals Under Conservatorship

- III. Summary of Proposed Rule

- A. Benchmark Levels for the Single-Family Housing Goals

- B. Proposed Alternatives to the Market-Based Retrospective Approach

- C. Multifamily Housing Goal Levels

- D. Small Multifamily Housing Subgoal Levels

- E. Single-Family Rental Housing

- F. Other Proposed Changes

- IV. Single-Family Housing Goals

- A. Factors Considered in Setting the Proposed Single-Family Housing Goal Levels

- B. Proposed Single-Family Benchmark Levels

- 1. Low-Income Home Purchase Goal

- 2. Very Low-Income Home Purchase Goal

- 3. Low-Income Areas Home Purchase Subgoal

- 4. Low-Income Areas Home Purchase Goal

- 5. Low-Income Refinancing Goal

- C. Proposed Alternatives to the Market-Based Retrospective Approach

- V. Multifamily Housing Goals

- A. Factors Considered in Setting the Proposed Multifamily Housing Goal Levels

- 1. The Multifamily Mortgage Market: Market Size, Competition and the Affordable Multifamily Market

- 2. Factors Impacting the Multifamily Mortgage Market

- 3. Enterprise Multifamily Performance

- 4. Ability of the Enterprises to Lead the Market in Making Multifamily Mortgage Credit Available and Need To Maintain Sound Financial Condition of the Enterprises

- B. Proposed Multifamily Housing Goal Benchmark Levels

- VI. Low-Income Housing Subgoal for Small Multifamily Properties

- A. Factors Considered in Setting the Proposed Levels for the Low-Income Housing Subgoal for Small Multifamily Properties

- 1. The Small Multifamily Market: Size, National Mortgage Credit Needs and Availability of Public Subsidies

- 2. Enterprise Small Multifamily Performance

- 3. Additional Factors: Ability of the Enterprises To Lead the Market in Making Small Multifamily Mortgage Credit Available and Need To Maintain Sound Financial Condition of the Enterprises

- B. Proposed Benchmark Levels for the Low-Income Housing Subgoal for Small Multifamily Properties

- VII. Reporting Requirements for Single-Family Rental Units

- VIII. Section-by-Section Analysis of Other Proposed Changes

- A. Changes to Definitions—Proposed § 1282.1

- 1. Definitions Related to Rent and Utilities

- 2. Definition of “Dwelling Unit”—Shared Living Arrangements

- 3. Additional Definition Changes

- B. Determining Affordability—Proposed § 1282.15

- 1. Use of Median Incomes

- 2. No Estimation of Affordability for Single-Family Owner-Occupied Units

- 3. Multifamily Affordability Based on Rents, Not Incomes

- 4. Reduced Cap on Estimating Affordability for Multifamily Properties

- 5. Reliance on Subsidy Program Requirements for Determining Affordability of Rents

- 6. Missing Bedroom Data

- 7. Changes To Reflect U.S. Census Bureau Terminology

- C. Skilled Nursing Units—Proposed § 1282.16(b)(15)

- D. Determining Affordability for Blanket Loans on Cooperative Housing—Proposed § 1282.16(c)(5)

- E. Seniors Housing—Proposed § 1282.16(c)(15)

- F. Mortgages With Unacceptable Terms or Conditions—Proposed § 1282.16(d)

- G. Housing Goals Guidance—Proposed § 1282.16(e)

- IX. Comments Requested on Specific Topics

- A. Blanket Loans on Manufactured Housing Parks

- B. Measurement of the Market

- X. Paperwork Reduction Act

- XI. Regulatory Flexibility Act

- List of Subjects in 12 CFR Part 1282

- Authority and Issuance

- CHAPTER XII—FEDERAL HOUSING FINANCE AGENCY

- Subchapter E—Housing Goals and Mission

- PART 1282—ENTERPRISE HOUSING GOALS AND MISSION

- Alternative 1—§ 1282.12

- Alternative 2—§ 1282.12

- Alternative 3—§ 1282.12

- Appendix: Additional Discussion Concerning The Proposed Single-Family Housing Goals

- I. Factors Considered in FHFA’s Market Models

- II. Additional Factors Considered

- III. The Performance and Effort of the Enterprises Toward Achieving the Single-Family Housing Goals in Previous Years and Future Market Estimates

- A. Enterprise Benchmark Levels and Performance: 2010-2013

- B. Projections From the Market Estimation Models

- Footnotes

Tables Back to Top

- Table 1—Government and Private Sector Market Share of Multifamily Originations

- Table 2—Enterprise Past Performance on the Low-Income Multifamily Goal, 2006-13

- Table 3—Enterprise Past Performance on the Very Low-Income Multifamily Subgoal, 2006-13

- Table 4—Enterprise Funding of Low-Income Units in Small Multifamily Properties, 2006-13

- Table 6—Enterprise Past Performance on the Low-Income Home Purchase Goal, 2006-13

- Table 7—Enterprise Past Performance on the Very Low-Income Home Purchase Goal, 2006-13

- Table 8—Enterprise Past Performance on the Low-Income Areas Home Purchase Goal and Subgoal, 2010-13

- Table 9—Enterprise Past Performance on the Low-Income Refinances Goal, 2010-13

DATES: Back to Top

FHFA will accept written comments on the proposed rule on or before October 28, 2014.

ADDRESSES: Back to Top

You may submit your comments on the proposed rule, identified by regulatory information number (RIN) 2590-AA65, by any one of the following methods:

- Agency Web site: www.fhfa.gov/open-for-comment-or-input.

- Federal eRulemaking Portal: http://www.regulations.gov. Follow the instructions for submitting comments. If you submit your comment to the Federal eRulemaking Portal, please also send it by email to FHFA at RegComments@fhfa.gov to ensure timely receipt by FHFA. Include the following information in the subject line of your submission: Comments/RIN 2590-AA65.

- Hand Delivered/Courier: The hand delivery address is: Alfred M. Pollard, General Counsel, Attention: Comments/RIN 2590-AA65, Federal Housing Finance Agency, Eighth Floor, 400 Seventh Street SW., Washington, DC 20024. Deliver the package at the Seventh Street entrance Guard Desk, First Floor, on business days between 9 a.m. and 5 p.m.

- U.S. Mail, United Parcel Service, Federal Express, or Other Mail Service: The mailing address for comments is: Alfred M. Pollard, General Counsel, Attention: Comments/RIN 2590-AA65, Federal Housing Finance Agency, Eighth Floor, 400 Seventh Street SW., Washington, DC 20024. Please note that all mail sent to FHFA via U.S. Mail is routed through a national irradiation facility, a process that may delay delivery by approximately two weeks.

FOR FURTHER INFORMATION CONTACT: Back to Top

Dr. Nayantara Hensel, Associate Director, Division of Housing Mission and Goals, at (202) 649-3122; Michael Groarke, Senior Policy Analyst, Division of Housing Mission and Goals, at (202) 649-3125; Kevin Sheehan, Office of General Counsel, at (202) 649-3086. These are not toll-free numbers. The mailing address for each contact is: Federal Housing Finance Agency, 400 Seventh Street SW., Washington, DC 20024. The telephone number for the Telecommunications Device for the Deaf is (800) 877-8339.

SUPPLEMENTARY INFORMATION: Back to Top

I. Comments Back to Top

FHFA invites comments on all aspects of the proposed rule, and will take all comments into consideration before issuing the final regulation. Copies of all comments will be posted without change, including any personal information you provide such as your name, address, email address and telephone number, on the FHFA Web site at http://www.fhfa.gov. In addition, copies of all comments received will be available for examination by the public on business days between the hours of 10 a.m. and 3 p.m., at the Federal Housing Finance Agency, 400 Seventh Street SW., Washington, DC 20024. To make an appointment to inspect comments, please call the Office of General Counsel at (202) 649-3804.

Commenters are encouraged to review and comment on all aspects of the proposed rule, including the single-family benchmark levels, the possible changes to the retrospective market approach, the multifamily benchmark levels, the new low-income housing subgoal for small multifamily properties, and other changes to the regulation. FHFA also requests comments on the two issues described in Section IX.

II. Background Back to Top

A. Statutory and Regulatory Background for the Existing Housing Goals

The Safety and Soundness Act requires FHFA to establish several annual housing goals for both single-family and multifamily mortgages purchased by Fannie Mae and Freddie Mac.

[1]

The annual housing goals are one measure of the extent to which the Enterprises are meeting their public purposes, which include “an affirmative obligation to facilitate the financing of affordable housing for low- and moderate-income families in a manner consistent with their overall public purposes, while maintaining a strong financial condition and a reasonable economic return.”

[2]

The housing goals provisions of the Safety and Soundness Act were substantially revised in 2008 with the enactment of the Housing and Economic Recovery Act, which amended the Safety and Soundness Act.

[3]

Under this revised structure, FHFA established housing goals for the Enterprises for 2010 and 2011 in a final rule published on September 14, 2010.

[4]

FHFA established new housing goals levels for the Enterprises for 2012 through 2014 in a final rule published on November 13, 2012.

[5]

The housing goals established by FHFA in these two prior rulemakings include four goals and one subgoal for single-family, owner-occupied housing and one goal and one subgoal for multifamily housing.

Single-family goals. The single-family goals defined under the Safety and Soundness Act include separate categories for home purchase mortgages for low-income families, very low-income families, and families that reside in low-income areas. Performance on the single-family home purchase goals is measured as the percentage of the total home purchase mortgages purchased by an Enterprise each year that qualifies for each goal or subgoal. There is also a separate goal for refinancing mortgages for low-income families, and performance on the refinancing goal is determined in a similar way.

Under the Safety and Soundness Act, the single-family housing goals are limited to mortgages on owner-occupied housing with one to four units total. The single-family goals cover “conventional, conforming mortgages,” with the “conventional” component meaning not insured or guaranteed by the Federal Housing Administration or other government agency and the “conforming” component meaning those mortgages with a principal balance that does not exceed the loan limits for Enterprise mortgages.

The single-family goals established by FHFA in 2010 and 2012 compare the goal-qualifying share of the Enterprise’s mortgage purchases to two separate measures: a “benchmark level” and a “market level.” The “benchmark level” is set prospectively by rulemaking, based on various factors, including FHFA’s forecast of the goal-qualifying share of the overall market. The “market level” is determined retrospectively each year, based on the actual goal-qualifying share of the overall market as measured by the Home Mortgage Disclosure Act (HMDA) data for that year. The “overall market” that FHFA uses for purposes of both the prospective market forecasts and the retrospective market measurement consists of all single-family owner-occupied conventional conforming mortgages that would be eligible for purchase by either Enterprise. It includes loans actually purchased by the Enterprises as well as comparable loans held in a lender’s portfolio. It also includes any loans that are part of a private label security (PLS), though very few such securities have been issued for conventional conforming mortgages since 2008.

Under this two-part approach, determining whether an Enterprise has met the single-family goal requirements for a specified year requires looking at both the benchmark level and the market level measures. In order to meet a single-family housing goal or subgoal, the actual percentage of mortgage purchases by an Enterprise that meet each goal or subgoal must exceed either the benchmark level or the market level for that year.

Multifamily goals. The multifamily goals defined under the Safety and Soundness Act include separate categories for mortgages on multifamily properties (i.e., properties with five or more units) with rental units affordable to low-income families and very low-income families. The multifamily goals established by FHFA in 2010 and 2012, as required by the Safety and Soundness Act, evaluate the performance of the Enterprises based on numeric targets, not percentages, for the number of affordable units in properties backed by mortgages purchased by an Enterprise. FHFA has not established a retrospective market level measure for the multifamily goals and subgoals, due to a lack of comprehensive data about the multifamily market such as that provided by HMDA for single-family mortgages. As a result, FHFA measures Enterprise multifamily goals performance against the benchmark levels only.

B. Adjusting the Housing Goals

Under the housing goals regulation first established by FHFA in 2010, as well as under this proposed rule, FHFA may adjust the benchmark levels for any of the single-family or multifamily housing goals in a particular year without going through notice and comment rulemaking based on (1) market and economic conditions or the financial condition of the Enterprise, or (2) a determination by FHFA that “efforts to meet the goal or subgoal would result in the constraint of liquidity, over-investment in certain market segments, or other consequences contrary to the intent of the Safety and Soundness Act or the purposes of the Charter Acts.”

[6]

The regulation also takes into account the possibility that achievement of a particular housing goal may or may not have been feasible for the Enterprise. If FHFA determines that a housing goal was not feasible for the Enterprise to achieve, then the regulation provides for no further enforcement of that housing goal for that year.

[7]

If, after publication of a final rule establishing the housing goals for 2015 through 2017, FHFA determines that any of the single-family or multifamily housing goals should be adjusted in light of market conditions, to ensure the safety and soundness of the Enterprises, or for any other reason, FHFA will take any steps that are necessary and appropriate to adjust that goal. Such steps could include adjusting the benchmark levels through the processes in the existing regulation or establishing new or revised housing goal levels through notice and comment rulemaking.

C. Housing Goals Under Conservatorship

On September 6, 2008, FHFA placed each Enterprise into conservatorship. Although the Enterprises remain in conservatorship at this time, they continue to have the mission of supporting a stable and liquid national market for residential mortgage financing. FHFA has continued to establish annual housing goals for the Enterprises and to assess their performance under the housing goals each year during conservatorship.

III. Summary of Proposed Rule Back to Top

A. Benchmark Levels for the Single-Family Housing Goals

This proposed rule would establish the benchmark levels for the single-family housing goals and subgoal for 2015-2017 as follows:

| Goal | Criteria | Current benchmark level for 2012-2014 (percent) | Proposed benchmark level for 2015-2017 (percent) |

|---|---|---|---|

| Low-Income Home Purchase Goal | Home purchase mortgages on single-family, owner-occupied properties with borrowers with incomes no greater than 80 percent of area median income | 23 | 23 |

| Very Low-Income Home Purchase Goal | Home purchase mortgages on single-family, owner-occupied properties with borrowers with incomes no greater than 50 percent of area median income | 7 | 7 |

| Low-Income Areas Home Purchase Subgoal | Home purchase mortgages on single-family, owner-occupied properties with: • Borrowers in census tracts with tract median income of no greater than 80 percent of area median income; and • Borrowers with income no greater than 100 percent of area median income in census tracts where (i) tract income is less than 100 percent of area median income, and (ii) minorities comprise at least 30 percent of the tract population. | 11 | 14 |

| Low-Income Refinancing Goal | Refinancing mortgages on single-family, owner-occupied properties with borrowers with incomes no greater than 80 percent of area median income | 20 | 27 |

B. Proposed Alternatives to the Market-Based Retrospective Approach

The proposed rule would adopt one of three different approaches for determining whether an Enterprise has met one of the single-family housing goals. Under the current regulation, the performance of the Enterprise on each single-family housing goal is compared to both a benchmark level and a retrospective market level. The first proposed alternative would maintain this approach. The second proposed alternative would evaluate the performance of the Enterprise based solely on a comparison to a benchmark level. The third proposed alternative would evaluate the performance of the Enterprise based solely on a comparison to a retrospective market level.

C. Multifamily Housing Goal Levels

The proposed rule would establish the levels for the multifamily goal and subgoal for 2015-2017 as follows:

| Goal | Criteria | Current goal levels for 2014 (units) | Proposed goal levels for 2015 (units) | Proposed goal levels for 2016 (units) | Proposed goal levels for 2017 (units) |

|---|---|---|---|---|---|

| Low-Income Goal | Units affordable to families with incomes no greater than 80 percent of area median income in multifamily rental properties with mortgages purchased by an Enterprise | Fannie Mae: 250,000 Freddie Mac: 200,000 | Fannie Mae: 250,000 Freddie Mac: 210,000 | Fannie Mae: 250,000 Freddie Mac: 220,000 | Fannie Mae: 250,000. Freddie Mac: 230,000. |

| Very Low-Income Subgoal | Units affordable to families with incomes no greater than 50 percent of area median income in multifamily rental properties with mortgages purchased by an Enterprise | Fannie Mae: 60,000 Freddie Mac: 40,000 | Fannie Mae: 60,000 Freddie Mac: 43,000 | Fannie Mae: 60,000 Freddie Mac: 46,000 | Fannie Mae: 60,000. Freddie Mac: 50,000. |

D. Small Multifamily Housing Subgoal Levels

The proposed rule would also establish for the first time a separate subgoal for rental units that are affordable to families with incomes no greater than 80 percent of area median income in small multifamily properties with mortgages purchased by an Enterprise. The proposed rule would establish the levels for the small multifamily subgoal for 2015-2017 as follows:

| Goal | Criteria | Current goal levels for 2014 (units) | Proposed goal levels for 2015 (units) | Proposed goal levels for 2016 (units) | Proposed goal levels for 2017 (units) |

|---|---|---|---|---|---|

| Low-Income Subgoal for Small Multifamily | Units affordable to families with incomes no greater than 80 percent of area median income in small multifamily rental properties (5 to 50 units) with mortgages purchased by an Enterprise | None | Fannie Mae: 20,000 Freddie Mac: 5,000 | Fannie Mae: 25,000 Freddie Mac: 10,000 | Fannie Mae: 30,000. Freddie Mac: 15,000. |

E. Single-Family Rental Housing

The housing goals regulation currently requires the Enterprises to report to FHFA on all mortgage purchases. Starting in 2015, FHFA plans to revise the reports required under this existing authority so that the Enterprises provide more detailed information about their purchases of mortgages on single-family rental housing, including detailed affordability information.

F. Other Proposed Changes

The proposed rule would also make a number of changes and clarifications to the existing rules concerning whether a particular mortgage purchase may be counted for purposes of the housing goals. These changes include updating and clarifying definitions and other provisions to reflect current Enterprise lending programs and market practices. The proposed rule would incorporate existing FHFA guidance on the appropriate treatment of loans on senior housing and skilled nursing units. The proposed rule would also add transparency to agency guidance on issues that may arise under the housing goals by placing past and future guidance on the FHFA Web site.

IV. Single-Family Housing Goals Back to Top

A. Factors Considered in Setting the Proposed Single-Family Housing Goal Levels

Section 1332(e)(2) of the Safety and Soundness Act requires FHFA to consider the following seven factors in setting the single-family housing goals:

1. National housing needs;

2. Economic, housing, and demographic conditions, including expected market developments;

3. The performance and effort of the Enterprises toward achieving the housing goals under this section in previous years;

4. The ability of the Enterprise to lead the industry in making mortgage credit available;

5. Such other reliable mortgage data as may be available;

6. The size of the purchase money conventional mortgage market, or refinance conventional mortgage market, as applicable, serving each of the types of families described, relative to the size of the overall purchase money mortgage market or the overall refinance mortgage market, respectively; and

7. The need to maintain the sound financial condition of the Enterprises.

[8]

FHFA has considered each of these seven statutory factors in setting the proposed benchmark levels for each of the single-family housing goals and subgoal. Additional discussion of these single-family factors is contained in the Appendix.

Market estimation models. In setting the proposed benchmark levels, FHFA relies extensively on its projections of the estimated market performance for each goal or subgoal in the primary mortgage market. FHFA has developed market estimation models for determining these projections. Additional discussion of the market estimation models can be found in a research paper, available at http://www.fhfa.gov/PolicyProgramsResearch/Research/.

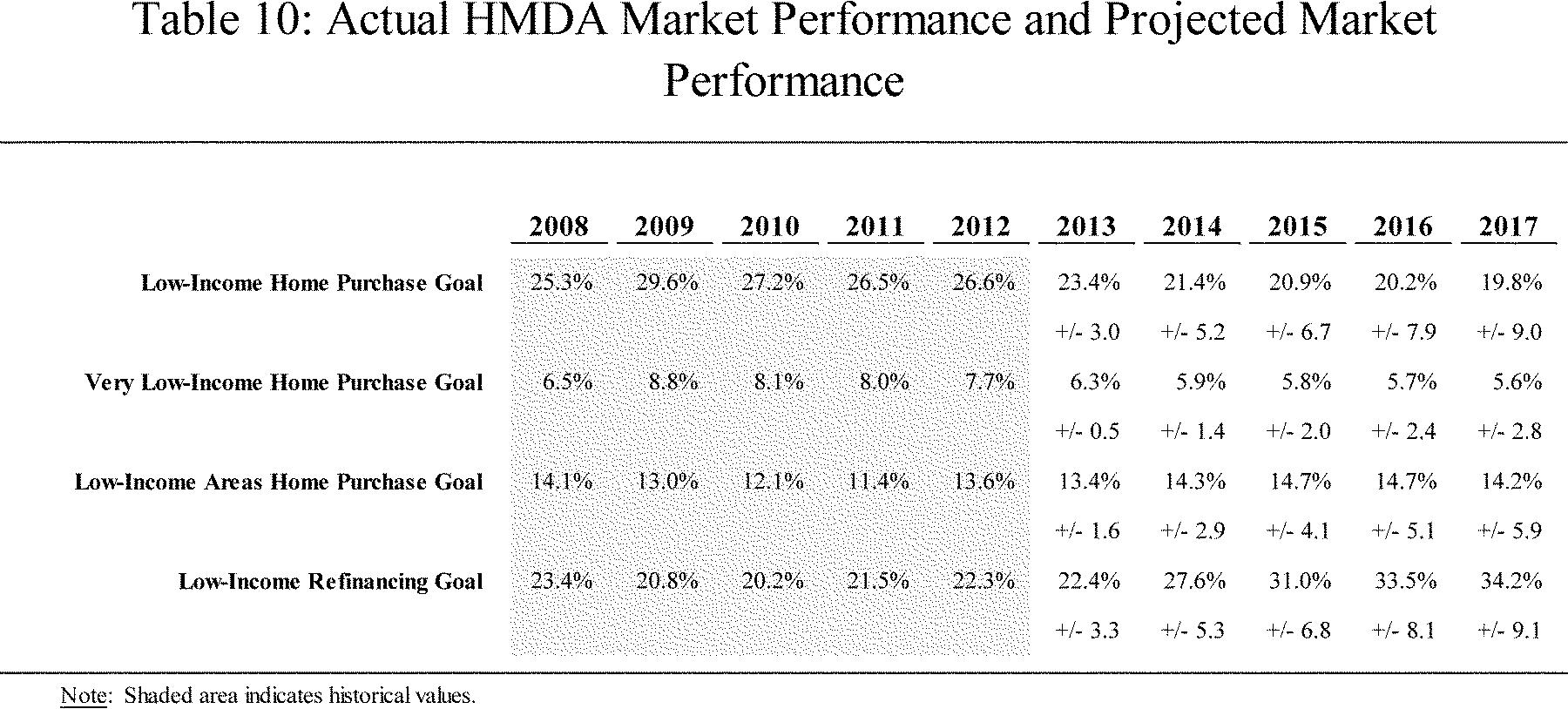

FHFA’s market estimation models look at the relationship between (a) the actual historical market performance for each single-family housing goal, as calculated from HMDA data, and (b) the actual historical values for various factors that may influence the market performance, such as interest rates, inflation, house prices, home sales and the unemployment rate. The market estimation models then use forecasts for each of the variables influencing market performance to project an estimated market performance for each goal or subgoal. The models yield a point estimate which represents the best estimate of goal qualifying shares for each year (i.e., 2015, 2016, and 2017), as well as a range of predicted levels based on different confidence levels. The models produce ranges and estimates for each successive year. For example, the estimate for the low-income home purchase goal for 2015 is 20.9 percent, with a 95 percent confidence interval of plus or minus 6.7 percent. In other words, the model prediction is that there is a 95 percent chance that the actual market share in 2015 will be between 14.2 percent and 27.6 percent. The same forecast for 2017 is 19.8 percent, with a 95 percent confidence interval of plus or minus 9.0 percent. Thus, the model prediction range for 2017 is between 10.8 percent and 28.8 percent.

FHFA periodically updates the market estimation models to reflect new data. These updates may result in changes to the specific variables that are included in the model for each of the housing goals. The updates may also result in new estimates for the goal-qualifying share for one or more of the single-family housing goals. If the market estimation models are updated before publication of the final rule, FHFA will consider any such updates and the new estimates for the goal-qualifying shares of the market when establishing the benchmark levels for 2015 through 2017.

The market estimation models address four of the seven factors that FHFA is required to consider. The models are designed to measure the size of the single-family mortgage market (Factor 6), and in doing so they incorporate aspects of three of the other factors: Factor 1: National Housing Needs; Factor 2: Economic, Housing, and Demographic Conditions; and Factor 5: Other Mortgage Data. Information about economic and housing conditions, such as the unemployment rate, inflation, housing starts, home sales, and home prices are included in the market models, which estimate the market performance for 2015 through 2017. FHFA also considers various other mortgage data sources, including the Mortgage Bankers Association’s mortgage default survey, the National Association of Realtors’ Housing Affordability Index and Freddie Mac’s Primary Mortgage Market Survey.

Past performance. The past performance of the Enterprises on each of the single-family housing goals and subgoal, Factor 3 above, is also an important factor in setting the benchmark levels. Reviewing the actual performance of the Enterprises on each housing goal in previous years and comparing that performance to the performance of the overall market helps FHFA ensure that the benchmark levels are set at levels that are feasible for the Enterprises to achieve. For example, the market estimation models may not capture all of the factors that contribute to Enterprise performance, or FHFA’s measurements of the market using HMDA data may not reflect the exact portion of the market that is eligible for purchase by the Enterprises. FHFA may rely more heavily on past Enterprise performance if the market estimation model yields results that are far above, or far below, the past performance of either Enterprise on a housing goal.

Other factors. FHFA has also considered the remaining two statutory factors in proposing these single-family housing goals: Factor 4: Ability to Lead the Industry and Factor 7: Need to Maintain Sound Financial Condition. FHFA’s consideration of these factors takes into account the financial condition of the Enterprises, the importance of maintaining the Enterprises in sound and solvent financial condition, and the appropriate role of the Enterprises in relation to the overall mortgage market. The process of setting benchmark levels based on the recent performance of the Enterprises and on the past and expected performance of the overall market also contributes to FHFA’s consideration of these required statutory factors.

[9]

FHFA continues to monitor the activities of the Enterprises, both in FHFA’s capacity as safety and soundness regulator and as conservator. If necessary, FHFA will make any appropriate changes in the housing goals to ensure the continued safety and soundness of the Enterprises.

B. Proposed Single-Family Benchmark Levels

1. Low-Income Home Purchase Goal

The low-income home purchase goal is based on the percentage of all single-family, owner-occupied home purchase mortgages purchased by an Enterprise that are for low-income families, defined as families with incomes less than or equal to 80 percent of the area median income.

The proposed rule would set the annual low-income home purchase housing goal benchmark level for 2015 through 2017 at 23 percent, which would be unchanged from the current 2014 benchmark level. FHFA’s market model forecasts a declining proportion of home purchase mortgages for low-income families for these years. FHFA has not reduced the proposed benchmark level, however, in order to encourage the Enterprises to continue their efforts to promote safe and sustainable lending to low-income families. This may include any steps the Enterprises take to bring greater certainty to origination and servicing standards for lenders, any additional outreach to small and rural lenders and to state and local Housing Finance Agencies (HFAs), and any other efforts by the Enterprises to reach underserved creditworthy borrowers.

A summary of the past performance of the Enterprises on the low-income home purchase housing goal, including past benchmark levels and the size of the market in past years, appears in the Appendix in Table 6.

Market size. FHFA’s forecast for the low-income share of the overall market for home purchase mortgages for 2015 through 2017 starts with a point estimate of 20.9 percent for 2015 and declines to a point estimate of 19.8 percent for 2017. These forecasts are significantly lower than the actual low-income share of the overall market for home purchase mortgages in 2010 through 2012 and are somewhat lower than FHFA’s estimates of the low-income share of the market for 2013 and 2014. The actual low-income market shares for 2010 through 2012 are based on FHFA’s analysis of the most recent HMDA data available and start at 27.2 percent in 2010, declining to 26.5 percent in 2011, and remaining essentially the same at 26.6 percent in 2012. FHFA has estimated the actual market shares for 2013 and 2014 using the market estimation models, because HMDA data for those years are not yet available. FHFA estimates that the low-income share of the overall market declined to 23.4 percent in 2013 and FHFA forecasts a further decline to 21.4 percent for 2014.

Past performance. The performance of the Enterprises on the low-income home purchase goal has followed a similar pattern as the overall market performance on the goal since 2010. Fannie Mae’s performance on the low-income home purchase goal in 2010 was 25.1 percent and, in fact, increased slightly in 2011 and 2012. Fannie Mae’s performance then declined to 23.8 percent in 2013. Freddie Mac’s performance on the low-income home purchase goal in 2010 was 26.8 percent before declining to 23.3 percent in 2011, increasing to 24.4 percent in 2012, and declining to 21.8 percent in 2013.

Past benchmark levels. The benchmark level for the low-income home purchase housing goal in 2010 and 2011 was 27 percent. This level was very close to the actual low-income share of the overall market as measured by HMDA data for 2010 and 2011. The benchmark level for the low-income home purchase housing goal was lowered to 23 percent for 2012, 2013 and 2014. This new benchmark level was significantly lower than the actual low-income share of the overall market in 2012. FHFA estimates that the low-income share of the overall market was slightly higher than the benchmark level in 2013, and that the low-income share of the overall market will be below the 23 percent benchmark level in 2014.

Proposed benchmark levels. Although FHFA’s market estimation model forecasts further declines in the low-income share of the overall home purchase mortgage market, the proposed rule would maintain the existing benchmark level of 23 percent for 2015 through 2017. FHFA is proposing this benchmark level in light of the current two-part process for evaluating Enterprise performance on the single-family housing goals, using both a benchmark level and a retrospective market level. If FHFA adopts an alternative approach that relies solely on benchmark levels, as described below in Section IV.C, FHFA may adopt a benchmark level in the final rule that is lower than the proposed benchmark level of 23 percent.

The market estimation model forecasts a range of possible market levels and, while the proposed benchmark level of 23 percent is above the point estimates for each year from 2015 through 2017, the proposed benchmark level is within the confidence interval range for those years. In addition, while the forecast of the market level declines each year from 2015 through 2017, the point estimate for 2015 is subject to less uncertainty than the point estimate for 2017. This supports setting the proposed benchmark level closer to the somewhat higher market estimate for 2015 than the lower estimate for 2017. Finally, FHFA is proposing benchmark levels for the low-income home purchase housing goal that are somewhat higher in the forecast range to encourage the Enterprises to continue to find ways to support lower income borrowers, without compromising safe and sound lending standards. FHFA will continue to monitor the Enterprises in its capacities as regulator and as conservator, and if FHFA determines in later years that the benchmark level for the low-income home purchase housing goal is no longer feasible for the Enterprises to achieve in light of market conditions, or for any other reason, FHFA will take appropriate steps to adjust the benchmark level.

2. Very Low-Income Home Purchase Goal

The very low-income home purchase goal is based on the percentage of all single-family, owner-occupied home purchase mortgages purchased by an Enterprise that are for very low-income families, defined as families with incomes less than or equal to 50 percent of the area median income.

The proposed rule would set the annual very low-income home purchase housing goal benchmark level for 2015 through 2017 at 7 percent, which would be unchanged from the current 2014 benchmark level. FHFA’s market model forecasts a declining proportion of home purchase mortgages for very low-income families for these years. FHFA has not reduced the proposed benchmark level, however, in order to encourage the Enterprises to continue their efforts to promote safe and sustainable lending to very low-income families. This may include any steps the Enterprises take to bring greater certainty to origination and servicing standards for lenders, any additional outreach to small and rural lenders and to state and local Housing Finance Agencies (HFAs), and any other efforts by the Enterprises to reach underserved creditworthy borrowers.

A summary of the past performance of the Enterprises on the very low-income home purchase housing goal, including past benchmark levels and the size of the market in past years, appears in the Appendix in Table 7.

Market size. FHFA’s forecast for the very low-income share of the overall market for home purchase mortgages is almost the same for each year from 2015 through 2017: 5.8 percent for 2015, 5.7 percent for 2016, and 5.6 percent for 2017. These forecasts for the very low-income share of the overall market are lower than the actual very low-income shares of the overall market in 2010 through 2012 and are slightly lower than the estimated very low-income shares for 2013 and 2014. The actual very low-income market shares for 2010 through 2012 are based on FHFA’s analysis of the most recent HMDA data available: 8.1 percent in 2010, declining slightly to 8.0 percent in 2011 and 7.7 percent in 2012. FHFA estimates that the very low-income share of the overall market declined to 6.3 percent in 2013, and FHFA forecasts a further decline to 5.9 percent for 2014.

Past performance. The performance of the Enterprises on the very low-income home purchase housing goal was relatively stable between 2010 and 2012, before declining in 2013. Fannie Mae’s performance was 7.2 percent in 2010, 7.6 percent in 2011 and 7.3 percent in 2012, while Freddie Mac’s performance was 7.9 percent in 2010, 6.6 percent in 2011 and 7.1 percent in 2012. Both Enterprises performed at a lower level on the very low-income home purchase housing goal in 2013, with Fannie Mae at 6.0 percent and Freddie Mac at 5.5 percent.

Past benchmark levels. The benchmark level for the very low-income home purchase housing goal in 2010 and 2011 was 8 percent. This level was very close to the actual very low-income share of the overall market as measured by HMDA data for 2010 and 2011. The benchmark level for the very low-income home purchase housing goal was lowered to 7 percent for 2012, 2013 and 2014. This new benchmark level was slightly below the actual very low-income share of the overall market in 2012. FHFA estimates that the very low-income share of the overall market for 2013 and 2014 will be below the benchmark level of 7 percent.

Proposed benchmark levels. Although FHFA’s market estimation model forecasts the very low-income share of the overall market to be below the current benchmark level, the proposed rule would maintain the existing benchmark level of 7 percent for 2015 through 2017. FHFA is proposing this benchmark level in light of the current two-part process for evaluating Enterprise performance on the single-family housing goals, using both a benchmark level and a retrospective market level. If FHFA adopts an alternative approach that relies solely on benchmark levels, as described below in Section IV.C, FHFA may adopt a benchmark level in the final rule that is lower than the proposed benchmark level of 7 percent.

The market estimation model forecasts a range of possible market levels and, while the proposed benchmark level is above the point estimates for each year from 2015 through 2017, the proposed benchmark level is within the confidence interval range for those years. FHFA is proposing benchmark levels for the very low-income home purchase housing goal that are somewhat higher in the forecast range to encourage the Enterprises to continue to find ways to support lower income borrowers, without compromising safe and sound lending standards. FHFA will continue to monitor the Enterprises in its capacities as regulator and as conservator, and if FHFA determines in later years that the benchmark level for the very low-income home purchase housing goal is no longer feasible for the Enterprises to achieve in light of market conditions, or for any other reason, FHFA will take appropriate steps to adjust the benchmark level.

3. Low-Income Areas Home Purchase Subgoal

The low-income areas home purchase subgoal is based on the percentage of all single-family, owner-occupied home purchase mortgages purchased by an Enterprise that are either: (1) For families in low-income areas, defined to include census tracts with median income less than or equal to 80 percent of area median income; or (2) for families with incomes less than or equal to area median income who reside in minority census tracts (defined as census tracts with a minority population of at least 30 percent and a tract median income of less than 100 percent of the area median income).

The proposed rule would set the annual low-income areas home purchase subgoal benchmark level for 2015 through 2017 at 14 percent. This proposed benchmark level would be an increase over the current benchmark level of 11 percent. However, the proposed benchmark level would be in line with FHFA’s forecasts for the actual low-income areas shares of the overall market and in line with the recent performance of the Enterprises on the low-income areas home purchase housing subgoal.

A summary of the past performance of the Enterprises on the low-income areas home purchase subgoal, including past benchmark levels and the size of the market in past years, appears in the Appendix in Table 8.

Market size. FHFA’s forecast for the low-income areas share of the overall market for home purchase mortgages is almost the same for each year from 2015 through 2017: 14.7 percent for 2015 and 2016, and 14.2 percent for 2017. These forecasts for the low-income areas share of the overall market are higher than the actual low-income areas shares of the overall market in 2010 through 2012, and are close to or higher than the estimated low-income areas shares for 2013 and 2014. The actual low-income areas market shares for 2010 through 2012 are based on FHFA’s analysis of the most recent HMDA data available: 12.1 percent in 2010, declining slightly to 11.4 percent in 2011 before increasing to 13.6 percent in 2012. FHFA estimates that the low-income areas share of the overall market increased to 13.4 percent in 2013, and FHFA forecasts a further increase to 14.3 percent for 2014.

Past performance. The performance of the Enterprises on the low-income areas home purchase subgoal has generally followed the changes in the low-income shares of the overall market between 2010 and 2013. Fannie Mae’s performance was 12.4 percent in 2010 and declined to 11.6 percent in 2011 before increasing to 13.1 percent in 2012 and 14.0 percent in 2013. Freddie Mac’s performance has followed the same basic pattern. Freddie Mac’s performance was 10.4 percent in 2010 and declined to 9.2 percent in 2011 before increasing to 11.4 percent in 2012 and 12.3 percent in 2013.

Past benchmark levels. The benchmark level for the low-income areas home purchase subgoal in 2010 and 2011 was 13 percent. This level was somewhat higher than the actual low-income areas share of the overall market as measured by HMDA data for 2010 and 2011. The benchmark level for the low-income areas home purchase subgoal was lowered to 11 percent for 2012, 2013 and 2014. This new benchmark level turned out to be lower than the actual low-income areas share of the overall market in 2012. FHFA estimates that the low-income areas share of the overall market for 2013 and 2014 will continue to be higher than the 2014 benchmark level of 11 percent.

Proposed benchmark levels. The proposed rule would set the annual low-income areas home purchase subgoal benchmark level for 2015 through 2017 at 14 percent. The proposed benchmark levels are higher than the current benchmark level of 11 percent. However, the proposed benchmark levels are very close to the low-income areas shares of the overall market forecast by FHFA’s market estimation model for 2015 through 2017, as well as to the recent performance levels of the Enterprises.

FHFA is proposing this benchmark level in light of the current two-part process for evaluating Enterprise performance on the single-family housing goals, using both a benchmark level and a retrospective market level. If FHFA adopts an alternative approach that relies solely on benchmark levels, as described below in Section IV.C, FHFA may adopt a benchmark level in the final rule that is lower than the proposed benchmark level of 14 percent. FHFA will continue to monitor the Enterprises in its capacities as regulator and as conservator, and if FHFA determines in later years that the benchmark level for the low-income areas home purchase housing goal is no longer feasible for the Enterprises to achieve in light of market conditions, or for any other reason, FHFA will take appropriate steps to adjust the benchmark level.

4. Low-Income Areas Home Purchase Goal

The low-income areas home purchase goal covers the same categories as the low-income areas home purchase subgoal, but it also includes moderate income families in designated disaster areas. As a result, the low-income areas home purchase goal is based on the percentage of all single-family, owner-occupied home purchase mortgages purchased by an Enterprise that are: (1) For families in low-income areas, defined to include census tracts with median income less than or equal to 80 percent of area median income; (2) for families with incomes less than or equal to median income who reside in minority census tracts (defined as census tracts with a minority population of at least 30 percent and a tract median income of less than 100 percent of the area median income); or (3) for families with incomes less than or equal to median income who reside in designated disaster areas.

The low-income areas goal benchmark level is established by a two-step process. The first step is setting the benchmark level for the low-income areas subgoal, which would be established by this proposed rule. The second step is establishing an additional increment for mortgages to families with incomes less than or equal to the area median income who are located in Federally-declared disaster areas. The disaster areas increment is set annually by FHFA separately from this rulemaking. Each year, FHFA notifies the Enterprises by letter of the benchmark level for that year. Thus, under this process, this proposed rule would set the annual low-income areas home purchase goal benchmark level for 2015 through 2017 at the subgoal benchmark level of 14 percent plus a disaster areas increment that FHFA will set separately and that may vary from year to year.

5. Low-Income Refinancing Goal

The low-income refinancing goal is based on the percentage of all single-family, owner-occupied refinancing mortgages purchased by an Enterprise that are for low-income families, defined as families with incomes less than or equal to 80 percent of the area median income.

The proposed rule would set the annual low-income refinancing housing goal benchmark level for 2015 through 2017 at 27 percent. This proposed benchmark level would be a significant increase from the current benchmark level of 20 percent. However, because FHFA forecasts even larger increases in the low-income share of the overall refinancing mortgage market, the proposed benchmark levels are relatively low in the forecast range for the low-income refinancing housing goal.

A summary of the past performance of the Enterprises on the low-income refinancing housing goal, including past benchmark levels and the size of the market in past years, appears in the Appendix in Table 9.

Market size. FHFA’s forecast for the low-income share of the overall market for refinancing mortgages in 2015 is 31.0 percent, increasing to 33.5 percent in 2016 and to 34.2 percent in 2017. These forecasts for the low-income share of the overall market for refinancing mortgages are notably higher than the actual low-income share in recent years. The actual low-income shares are based on FHFA’s analysis of the most recent HMDA data available. The low-income share of the overall refinancing mortgage market in 2010 was 20.2 percent, increasing slightly to 21.5 percent in 2011 and to 22.3 percent in 2012. FHFA estimates that the low-income share of the overall refinancing market increased slightly to 22.4 percent in 2013, and FHFA forecasts a more significant increase for 2014, to 27.6 percent.

Past performance. The performance of the Enterprises on the low-income refinancing housing goal was somewhat higher than the actual market levels for 2010 through 2012, as well as the forecast market level for 2013. Since 2010, the low-income refinancing housing goal has treated modifications under the Home Affordable Modification Program (HAMP) as refinancing mortgages for purposes of the housing goals. The Enterprise performance numbers include HAMP modifications, which are not included in the data used to calculate the market levels. Including HAMP modifications in the Enterprise performance numbers tends to increase the measured performance of the Enterprises on the low-income refinancing housing goal. This is because lower income borrowers make up a greater proportion of the borrowers receiving HAMP modifications than the low-income share of the overall refinancing mortgage market.

Fannie Mae’s performance on the low-income refinancing housing goal was 20.9 percent in 2010, increasing to 23.1 percent in 2011, falling to 21.8 percent in 2012, and increasing again to 24.3 percent in 2013. Freddie Mac’s performance followed a similar pattern, starting at 22.0 percent in 2010, increasing to 23.4 percent in 2011, falling to 22.4 percent in 2012, and increasing again to 24.1 percent in 2013.

Past benchmark levels. The benchmark level for the low-income refinancing housing goal was 21 percent in 2010 and 2011. This level was very close to the actual low-income share of the overall refinancing mortgage market as measured by HMDA data for 2010 and 2011. The benchmark level for the low-income refinancing housing goal was lowered to 20 percent for 2012, 2013 and 2014. This new benchmark level was below the actual low-income share of the overall refinancing mortgage market in 2012. FHFA estimates that the low-income share of the overall refinancing mortgage market for 2013 and 2014 will be significantly higher than the benchmark level of 20 percent.

Proposed benchmark levels. The proposed rule would set the annual low-income refinancing housing goal benchmark level for 2015 through 2017 at 27 percent. This is significantly higher than the current benchmark level of 20 percent. FHFA’s market estimation model forecasts the low-income share of the overall refinancing mortgage market to be significantly higher than both the current benchmark level and the recent performance of the Enterprises. Although the proposed rule would increase the benchmark level for the low-income refinancing goal significantly, the proposed benchmark levels would be lower than the point estimates projected by the market estimation model for 2015 through 2017. However, the proposed benchmark level would still be within the range of possible market levels forecast by the market estimation model. In addition, while the forecast of the market level increases each year from 2015 through 2017, the point estimate for 2015 is subject to less uncertainty than the point estimate for 2017. This supports setting the proposed benchmark level closer to the somewhat lower market estimate for 2015 than the higher estimate for 2017.

Although this proposed benchmark level is higher than any level achieved by either Enterprise since 2010 and would represent an increase of 7 percentage points over the current goal, the proposed benchmark level should be achievable because higher income borrowers are historically more likely to refinance their mortgages when interest rates have decreased. As a result, when interest rates fall, overall refinance volumes tend to increase, but the low-income goal qualifying share tends to decrease. The opposite is true when interest rates increase: There are usually fewer refinancings overall, but a greater percentage of those refinancings are by low-income borrowers. FHFA’s market model forecasts that over the next three years the low-income goal-qualifying share of refinancing mortgages will increase significantly both due to future increases in interest rates and due to the fact that many borrowers would already have refinanced during the recent extended period of historically low interest rates.

FHFA is proposing this benchmark level in light of the current two-part process for evaluating Enterprise performance on the single-family housing goals, using both a benchmark level and a retrospective market level. If FHFA adopts an alternative approach that relies solely on benchmark levels, as described below in Section IV.C, FHFA may adopt a benchmark level in the final rule that is lower than the proposed benchmark level of 27 percent. In addition, FHFA will continue to monitor the Enterprises in its capacities as regulator and as conservator, and if FHFA determines in later years that the benchmark level for the low-income refinancing housing goal is no longer feasible for the Enterprises to achieve in light of market conditions, or for any other reason, FHFA will take appropriate steps to adjust the benchmark level.

C. Proposed Alternatives to the Market-Based Retrospective Approach

Since 2010, the single-family housing goals have measured Enterprise performance by comparing it to both: (1) A benchmark level that is set in advance, and (2) the actual market level, as measured retrospectively based on HMDA data. Under the current rule, an Enterprise has met a goal if it achieves either the benchmark level for that goal, or the actual, retrospective market size for that goal. FHFA is requesting comment on whether this current approach should be maintained or whether FHFA should adopt a different approach in the final rule.

FHFA is proposing three different alternatives and may adopt any of the three in the final rule. The first alternative would maintain the current approach, measuring performance on the single-family housing goals against both a benchmark level and a market level. The second alternative would eliminate the retrospective market level and measure performance on the single-family housing goals against a benchmark level only. The third alternative would eliminate the prospective benchmark levels and measure performance on the single-family housing goals against a retrospective market level only.

Each of these alternatives strikes a different balance between goals that are established in advance and goals that are determined retrospectively based on market performance. To the extent any of these alternatives sets goal levels in advance, it is easier for the Enterprises to establish plans for meeting the goal, while at the same time it is harder for FHFA to set the goal accurately for more than one year in advance. To the extent that an alternative sets goal levels retrospectively based on market performance, it is harder for the Enterprises to establish plans for meeting the goal, but the goal level is more likely to be feasible because it would be based on the actual performance of the overall market.

Under each of these alternatives, FHFA would continue to monitor the Enterprises in its capacities as regulator and as conservator. If FHFA determines that the housing goals established under any of these alternatives need to be adjusted in light of changes in the market, to ensure the safety and soundness of the Enterprises, or for any other reason, FHFA will take all appropriate steps, including adjusting the levels of the housing goals or initiating additional rulemaking to amend the housing goals regulation.

Alternative 1: Benchmark Level and Market Level. The first alternative being proposed by FHFA would continue evaluating Enterprise performance based on a comparison with both a benchmark level that is set prospectively by regulation and a retrospective market level based on HMDA data.

This alternative would maintain the existing regulatory language in § 1282.12. Paragraph (a) would continue to provide that “[a]n Enterprise shall be in compliance with a single-family housing goal if its performance under the housing goal meets or exceeds either: (1) The share of the market that qualifies for the goal; or (2) The benchmark level for the goal.” Paragraph (b) would define the process for measuring the share of the market that qualifies for the goal. The remaining paragraphs in the section would describe each of the single-family housing goals, including the retrospective market share and the benchmark level, where applicable.

This two-part approach incorporates some of the advantages both of a benchmark level that is set prospectively and of a market level that is set retrospectively. By including a benchmark level, the two-part approach gives the Enterprises more certainty in planning how they will achieve the single-family housing goals each year. At the same time, the retrospective market level measure helps to address the inherent difficulty of accurately forecasting, years in advance, the housing goals shares of the overall market. The retrospective market level is much more adaptive than a fixed benchmark level by itself, although the HMDA data used for the retrospective measure does not become available until September of the following year. The retrospective market level incorporates many of the same considerations that FHFA uses in setting the prospective benchmark levels, but it is based on the actual performance of the market in the year being evaluated. This versatility helps ensure that the single-family goals are feasible for the Enterprises to achieve each year. Without the retrospective market approach, additional regulatory action would be required for the agency to adapt to unanticipated market changes.

One disadvantage of this two-part approach is that if the Enterprises anticipate that the retrospective market level will end up lower than the benchmark level for a particular year, the single-family housing goals may provide less of an incentive for the Enterprises to serve the targeted parts of the market. On the other hand, the Enterprise would still have some incentive to meet benchmark targets in the first instance, rather than waiting to find out the results of the market-based analysis.

Another potential disadvantage of the retrospective, market-based approach generally is that it may be less meaningful under market circumstances where the Enterprises purchase a large percentage of the total number of single-family, conventional conforming mortgages in a particular year. In those circumstances, the retrospective, market-based approach would effectively compare the performance of the Enterprises to their own activity.

FHFA welcomes comments on this alternative, including any other advantages or disadvantages of measuring performance against both a benchmark level and the market level.

Alternative 2: Benchmarks Only. The second alternative being proposed by FHFA would be to evaluate Enterprise performance on the single-family housing goals based solely on a comparison with a benchmark level that is set prospectively by regulation.

[10]

This alternative would revise the existing regulatory language in § 1282.12(a) to provide that “[a]n Enterprise shall be in compliance with a single-family housing goal if its performance under the housing goal meets or exceeds the benchmark level for the goal.” The current paragraph (b) would be deleted from the regulation. The remaining paragraphs in the section would be revised to delete from each the current subparagraph (1), which refers back to the retrospective market level. As revised, these paragraphs would simply set out the benchmark levels for each of the single-family housing goals.

An advantage of this approach is that it would provide the Enterprises with certainty in planning how to achieve the single-family housing goals each year. Another advantage of this approach would be that FHFA could determine whether the Enterprises met the single-family goals relatively early in the year, allowing the Enterprises to adjust their activities if necessary.

A disadvantage of the benchmarks-only approach is the difficulty in accurately forecasting market dynamics and goal-qualifying share levels years in advance. As a result, much of the impact of using housing goals based only on prospective benchmark levels depends on whether those forecasts are accurate or if the actual market level for that year is higher or lower than the benchmark level. If the actual market level for a particular year turns out to be higher than the benchmark level that was set in advance, the Enterprises are likely to find the goal easy to achieve without a particular focus on serving the portions of the single-family market targeted by the housing goals. Conversely, if the actual market level for a particular year turns out to be lower than the benchmark level that was set in advance, the Enterprises may find the goal difficult or impossible to achieve.

If FHFA adopts this alternative, FHFA would consider whether adjustments to the proposed benchmark levels for the single-family housing goals are necessary. Without the existence of the retrospective market level to help mitigate the uncertainty in projecting the market shares for each goal, FHFA’s considerations might lead the agency to select a benchmark that is in the lower part of the projected market range.

FHFA welcomes comments on this alternative, including any other advantages or disadvantages of measuring performance against a benchmark level only. FHFA also encourages commenters to address what benchmark levels would be appropriate for each of the single-family housing goals if FHFA adopts this alternative in the final rule.

Alternative 3: Market Level Only. The third alternative being proposed by FHFA would be to evaluate Enterprise performance on the single-family housing goals based solely on a comparison with a retrospective market level based on HMDA data.

This alternative would revise the existing regulatory language in § 1282.12(a) to provide that “[a]n Enterprise shall be in compliance with a single-family housing goal if its performance under the housing goal meets or exceeds the share of the market that qualifies for the goal.” Paragraph (b) would define the process for measuring the share of the market that qualifies for the goal. The remaining paragraphs in the section would be revised to delete from each the current subparagraph (2), which sets out the benchmark level for each single-family housing goal.

Under this alternative, whether an Enterprise meets a particular housing goal would depend solely on whether the performance of the Enterprise met the actual market level for that year. This would eliminate the need for FHFA to forecast the goal-qualifying share of the overall market, and it would make it more likely that the single-family goals would be feasible for the Enterprises each year compared to Alternative 2. An additional advantage of this approach would be that it would require the Enterprises to continue efforts to support all aspects of the market in years when the actual market levels are higher than forecasts would have predicted.

A disadvantage of this approach would be that it may be more difficult for the Enterprises to establish plans for how to meet or exceed the actual market level. If FHFA adopts this alternative, it may be necessary for FHFA to require more frequent reporting from the Enterprises on their current activities and on their forecasts and plans for addressing the housing goals over the course of each year. As discussed under Alternative 1, another disadvantage of the retrospective, market-based approach is that it may be less meaningful under market circumstances where the Enterprises purchase a large percentage of mortgages in a particular year. In addition, this alternative would not allow FHFA to determine whether an Enterprise has met the single-family goals until October of the following year.

FHFA welcomes comments on this alternative, including other advantages or disadvantages of measuring performance against a market level that can only be determined retrospectively, or against a market level based on data from a previous year.

V. Multifamily Housing Goals Back to Top

A. Factors Considered in Setting the Proposed Multifamily Housing Goal Levels

Section 1333(a)(4) of the Safety and Soundness Act requires FHFA to consider the following six factors in setting the multifamily housing goals:

1. National multifamily mortgage credit needs and the ability of the Enterprise to provide additional liquidity and stability for the multifamily mortgage market;

2. The performance and effort of the Enterprise in making mortgage credit available for multifamily housing in previous years;

3. The size of the multifamily mortgage market for housing affordable to low-income and very low-income families, including the size of the multifamily markets for housing of a smaller or limited size;

4. The ability of the Enterprise to lead the market in making multifamily mortgage credit available, especially for multifamily housing affordable to low-income and very low-income families;

5. The availability of public subsidies; and

6. The need to maintain the sound financial condition of the Enterprise.

[11]

In setting the proposed benchmark levels for the multifamily housing goals, FHFA has considered each of the six statutory factors. The statutory factors for the multifamily goals are very similar, but not identical, to the statutory factors considered in setting the benchmark levels for the single-family housing goals. At the same time, there are several important distinctions between the single-family housing goals and the multifamily housing goals. While there are separate single-family housing goals for home purchase and refinancing mortgages, the multifamily goals include all Enterprise multifamily mortgage purchases, regardless of the purpose of the loan. In addition, unlike the single-family housing goals, by statute the multifamily goals are measured based on the total volume of affordable multifamily mortgage purchases, not based on a percentage of multifamily mortgage purchases. The use of total volumes, which FHFA measures by the number of eligible units, rather than percentages of each Enterprises’ overall multifamily purchases requires particular attention both to the overall size of the multifamily mortgage market and to the expected volume of the Enterprises’ multifamily purchases in a given year.

Another difference between the single-family and multifamily goals is that performance on the multifamily housing goals is measured based solely on a benchmark level, without any retrospective market measure. The absence of a retrospective market measure for the multifamily housing goals results, in part, from the lack of comprehensive data about the multifamily mortgage market. Unlike the single-family market, where HMDA provides a reasonably comprehensive dataset about single-family mortgage originations each year, the multifamily market (and the affordable multifamily market segment) has no such comparable data set. As a result, it can be difficult to correlate different data sets that may rely on different reporting formats—for example, some data is available by dollar volume while other data is available by unit production. The lack of comprehensive data about the multifamily mortgage market is even more acute with respect to the segments of the market that are targeted to low-income families, defined as families with incomes less than or equal to 80 percent of the area median income, and very low-income families, defined as families with incomes less than or equal to 50 percent of the area median income. Much of the analysis that follows discusses trends in the overall multifamily mortgage market. FHFA recognizes that these general trends may not apply to the same extent to all segments of the market.

FHFA has considered each of the required statutory factors and a discussion of the various factors, a number of which are related or overlap, follows.

1. The Multifamily Mortgage Market: Market Size, Competition and the Affordable Multifamily Market

FHFA’s consideration of the multifamily mortgage market addresses the size of and competition within the multifamily mortgage market, as well as the subset of the multifamily market affordable to low-income and very low-income families (Factors 1, 3 and 5). Recent trends in the multifamily market indicate that overall multifamily mortgage market volumes are expected to increase between 2014 and 2017, both in terms of total refinancing activity and total financing for new multifamily units being completed. However, FHFA expects the Enterprises will make up a smaller share of the overall multifamily mortgage market due to increased participation from the private sector. FHFA has also considered the importance of Enterprise support of the multifamily market in light of recent decreases in rental affordability.

Multifamily mortgage market size. The overall size of the multifamily market, in terms of units, was over 23 million rental units in 2011, according to the data from the U.S. Census Bureau in the 2011 American Community Survey (ACS).

[12]

The size of the multifamily market in terms of mortgage origination volume varies significantly from year to year based on a variety of market conditions.

During the financial crisis and the resulting decline in the housing market, the size of the multifamily mortgage market decreased significantly. Overall, multifamily mortgage originations fell from $147.7 billion in 2007 to $87.9 billion in 2008 and $52.5 billion in 2009, as shown in Table 1. The declines were even more pronounced in the private sector segment of the multifamily market, which decreased from almost $112 billion in 2007 to $46.4 billion in 2008 and $18.4 billion in 2009. The Enterprises’ multifamily purchases provided a countercyclical source of financing during this same period. While the size of the overall multifamily mortgage market was declining, the volume of Enterprise purchases was relatively steady. The combined volume of Enterprise purchases in 2007, excluding purchases of commercial mortgage-backed securities (CMBS), was $34.6 billion. The Enterprises’ combined multifamily volume rose to $40 billion in 2008 before declining to $31 billion in 2009.

| Year | Total volume S Bil. | % Fannie Mae | % Freddie Mac | % Enterprise total | % FHA | % Private sector |

|---|---|---|---|---|---|---|

| *FHA data is for fiscal year 2005 to 2013. | ||||||

| Sources: “MBA Commercial Real Estate Finance Survey.” | ||||||

| Sources for 2013 data: Fannie Mae, Freddie Mac, and FHA. Total 2013 volume derived from “MBA Commercial Real Estate Finance Survey” data. | ||||||

| Note: All multifamily loans in CMBS issuances are included under “Private Sector”, regardless of the investor. | ||||||

| 2005 | $133.1 | 11.7 | 6.7 | 18.4 | 2.2 | 79.3 |

| 2006 | 138.0 | 11.7 | 7.1 | 18.8 | 10 | 80.2 |

| 2007 | 147.7 | 13.1 | 10.4 | 23.4 | 0.8 | 75.8 |

| 2008 | 87.9 | 25.4 | 20.1 | 45.5 | 1.7 | 52.8 |

| 2009 | 52.5 | 30.2 | 28.9 | 59.2 | 5.6 | 35.2 |

| 2010 | 68.8 | 24.5 | 20.3 | 44.8 | 15.3 | 40.0 |

| 2011 | 110.1 | 20.9 | 18.9 | 39.8 | 10.6 | 49.6 |

| 2012 | 146.1 | 21.7 | 18.3 | 39.9 | 10.2 | 49.8 |

| 2013 | 170.0 | 16.6 | 14.8 | 31.4 | 10.4 | 58.3 |

Since 2009, the overall size of the market has rebounded and has shown increasing private sector participation. The market has increased from a low of $52.5 billion in 2009, to $69 billion in 2010, $110 billion in 2011, and $146 billion in 2012. Total multifamily mortgage originations from all capital sources continued to increase in 2013, to $170 billion.

[13]

Competition in the multifamily mortgage market. Increased demand for multifamily housing and strong investment returns have attracted banks, insurance companies, CMBS issuers, and other private lenders back to the multifamily market.

[14]

Much of the increase in private sector activity has come from commercial banks and life insurance companies, the entities, other than the Enterprises, that purchase the most multifamily mortgages. Additionally, multifamily loans included in CMBS issuances increased from $785 million in the first half of 2013 to $2.6 billion in the first half of 2014.

[15]

FHA also remained a significant backer of multifamily mortgages, insuring over $18 billion in multifamily loans in 2013.

[16]

As reflected in Table 1, increased competition in the multifamily mortgage market resulted in the Enterprises’ multifamily market share declining from a peak of almost 60 percent in 2009 to just under 40 percent in 2011 and 2012 and to just over 30 percent in 2013.

[17]

The decrease in market share for the Enterprises relative to the overall market is expected to continue in 2014 and beyond. According to the MBA multifamily originations index, total multifamily originations for the first quarter of 2014 were about the same as first quarter 2013 data. MBA data shows a sharp rise in multifamily lending by banks and life insurance companies from first quarter 2013 compared to first quarter 2014.

[18]

The increase in activity by banks and life insurance companies likely affected the Enterprises’ combined multifamily loan purchases, which were down by almost 50 percent in the first half of 2014 compared to their purchases in the first half of 2013. While this sharp decline is unlikely to continue through the rest of 2014, the overall trend of increased competition from the private sector is expected to continue in 2014 and beyond.

Affordable Multifamily Market Segment. FHFA’s consideration of the multifamily mortgage market is limited by the lack of comprehensive data about the size of the market for low-income and very low-income families. However, FHFA recognizes that the portion of the overall multifamily mortgage market that is affordable to low-income and very low-income families may vary from year-to-year, that the competition within the multifamily market overall may differ from the competition within the affordable multifamily market segment, and that the volume for the affordable multifamily market segment will also be related to the availability of affordable housing subsidies.

Affordability for families living in rental units has decreased in recent years for many households. Spending more than 30 percent of household income towards rent is often used as a measure of whether a household is rent burdened, and the Safety and Soundness Act also incorporates this metric when determining whether a unit meets the low-income or very low-income categories, with appropriate adjustments for unit size.

[19]

According to the Joint Center on Housing Studies, “[t]he share of cost-burdened renters increased in all but one year from 2001 to 2011, to just above 50 percent. More than a quarter of renter households (28 percent) had severe burdens (paid more than half their incomes for housing). In 2012, the share of cost-burdened renters improved slightly but their numbers held steady as more households entered the rental market.”

[20]

The affordable segment of the multifamily market is critical in meeting the housing needs of low-income and very low-income families that would otherwise be rent-burdened. Financing for affordable multifamily buildings—particularly those that are affordable to very low-income families, defined as families with incomes at or below 50 percent of AMI—often uses an array of state and federal housing subsidies, such as low-income housing tax credits (LIHTCs), tax-exempt bonds, Section 8 rental assistance or soft subordinate financing. Investor interest in tax credit equity projects of all types and in all markets is strong and is expected to remain so, especially in markets in which bank investors are seeking to meet Community Reinvestment Act (CRA) goals. Consequently, there should continue to be opportunities in the multifamily market to provide permanent financing for properties with low-income housing tax credits during the 2015-2017 period. Additionally, there should also be opportunities for market participants, including the Enterprises, to purchase mortgages that finance the preservation of existing affordable housing units (especially for restructurings of older properties that reach the end of their initial 15-year LIHTC compliance periods and for refinancing properties with expiring Section 8 rental assistance contracts).

2. Factors Impacting the Multifamily Mortgage Market

FHFA has considered a variety of economic indicators and measures related to the size and affordability of the multifamily mortgage market, which reflect fundamentals in the overall multifamily market and an ongoing need for affordable multifamily rental units. This section examines the following: interest rates, property values, multifamily rents, vacancy rates, multifamily building permits, multifamily housing starts, and multifamily housing completions.

Interest rates. The volume of multifamily mortgage originations is influenced heavily by interest rates. Although interest rates rose in 2013, they remained low compared to historical levels. If multifamily mortgage rates increase relative to the lower rates prior to 2013, multifamily mortgage origination volumes would be expected to decrease, including both refinancings and purchases.

Lower mortgage interest rates in recent years have resulted in refinancings making up a significant percentage of overall multifamily volume. This is reflected in the share of multifamily units financed by mortgages purchased by the Enterprises. For Fannie Mae, the share of multifamily units financed that were refinancings (as opposed to purchases, new construction, or preservation) increased from 64 percent in 2009, peaked at 75 percent in 2010, and declined to 66 percent in 2011, 66 percent in 2012, and 60 percent in 2013. For Freddie Mac the share of multifamily units financed that were refinancings declined from 77 percent in 2009, to 61 percent in 2010, 59 percent in 2011, 58 percent in 2012, and 50 percent in 2013.

[21]

If mortgage interest rates increase, the volume of refinancing mortgages can be expected to decrease.

In addition to the impact on refinancing volumes, increases in mortgage interest rates would make it more costly to finance the purchase of multifamily properties. The increased cost of multifamily financing would tend to decrease the volume of multifamily mortgage originations that fund purchases of multifamily properties.

Property values. As of the end of January 2014, multifamily property values were up over 13 percent from January 2013 and are now at or above the peak reached in 2007.

[22]

Rising multifamily property values usually spur increases in refinancings, property sales, and new construction activity. The impact of higher multifamily property values may be offset to some extent by rising interest rates. FHFA anticipates that multifamily property values will continue to increase in 2014, with more modest increases continuing during 2015-2017.

Multifamily vacancy rates and rents. During the housing crisis, vacancy rates for multifamily properties increased significantly and median asking rents declined. Since that time, vacancy rates have returned to lower levels, while rents have increased. Rental vacancy rates for multifamily units peaked at over 13 percent in the third quarter of 2009 but have declined each year since. Vacancy rates fell to around 9 percent in 2012 and have continued to average around 9 percent through 2013.

[23]

Median asking rents nationwide declined slightly between 2009 and 2011, from $708 in 2009 to $694 in 2011. Median asking rents have increased since 2011, reaching $734 in 2013 and $756 in the second quarter of 2014.

[24]

Both the average vacancy rates and median asking rents indicate that the market for multifamily housing will remain relatively strong, though trends in both measures are likely to moderate.

Multifamily building permits, starts and completions. Multifamily building permits and starts have recovered in recent years, after falling significantly after the housing market crisis. Multifamily building permits averaged 357,000 units annually between 2005 and 2008. The annual volume of multifamily building permits fell dramatically in 2009 and 2010, to approximately 130,000 units per year. The volume of permits has increased in the years since 2010, exceeding 340,000 units in 2013 and on pace to do the same in 2014.

[25]